1. What is Bill C-9: An Act to Amend the Income Tax Act (Canada Emergency Rent Subsidy and Canada Emergency Wage Subsidy)?

Bill C-9: An Act to Amend the Income Tax Act (Canada Emergency Rent Subsidy and Canada Emergency Wage Subsidy) (the “Bill”)[1] amends the Income Tax Act by introducing a new rent subsidy called the Canada Emergency Rent Subsidy (“CERS”). CERS replaces the former rent subsidy program known as Canada Emergency Commercial Rent Assistance (“CECRA”). The purpose of the Bill is to respond more effectively to the financial pressures that tenants experience as a result of the pandemic.

Formerly under CECRA, a landlord would have to agree for the tenant to apply for support. Now, under CERS, the tenant can apply for support directly through the Canada Revenue Agency, without involving the landlord. The Bill provides compensation to businesses that have struggled to pay certain expenses, such as rent, mortgage interest, insurance, and property taxes, due to the pandemic.

2. Who Is Eligible to Apply?

Any “qualifying renter” can apply for the subsidy. To classify as a qualifying renter, a tenant must satisfy itself of the following:

- The tenant is an “eligible entity,” which includes individuals and taxable corporations, along with other kinds of business organizations;[2] and

- The tenant fulfills the strict procedural requirements of the program. These include:

a. Filing an application with the Minister for the qualifying period within 180 days after the end of the qualifying period;

b. Ensuring that the person responsible for the tenant’s financials attests to the accuracy and completion of the application; and

c.. Meeting one of two criteria regarding payroll and the holding of a business number.[3]

The legislature may prescribe additional conditions that a tenant must satisfy in order to be or to remain a “qualifying renter.”

3. When Can a Tenant Apply?

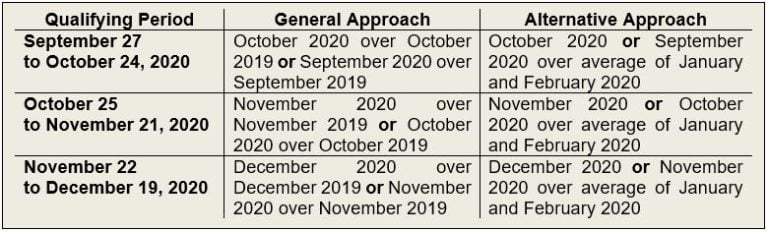

A tenant can apply for CERS for any of the following prescribed “qualifying periods:”

- September 27, 2020 to October 24, 2020;

- October 25, 2020 to November 21, 2020;

- November 22, 2020 to December 19, 2020; or

- A prescribed period that ends no later than June 30, 2021.[4]

The Bill is retroactively effective beginning September 27, 2020. The subsidy may be available until June 2021; however, the Bill has not outlined the dates of the qualifying periods running from December 19, 2020 to June 2021. Presumably, this is because the Minister will want to review the rate at which they are offering tenants support in light of any economic and public health developments after December 19, 2020.

The program link has not been made available yet. Once it is available, applicants can apply directly through the Canadian Revenue Agency, rather than through their landlords.

4. What Is Covered?

Qualifying Rent Expense

The subsidy covers a portion of an eligible entity’s “qualifying rent expense” in respect of a qualifying property, meaning real or immovable property in Canada that the eligible entity uses in the course of its ordinary activities.[5]

A qualifying rent expense is limited to expenses paid to a party at arm’s length under a written agreement entered into before October 9, 2020, or pursuant to a renewal (on substantially similar terms) or assignment of an agreement entered into before October 9, 2020. The list of eligible expenses is non-exhaustive and includes, for example, gross rent, but excludes a handful of other common expenses such as sales taxes.

For eligible entities that own qualifying property, the calculation also takes into account any commercial mortgage interest, insurance, and property taxes that the tenant owes on the land.

The Cap on Qualifying Rent Expenses

Qualifying rent expenses are capped at $75,000 for a single eligible entity. If an eligible entity’s qualifying rent expense exceeds $75,000, the eligible entity will therefore only be able to apply the subsidy to $75,000 worth of its qualifying rent expense.

Importantly, if a qualifying renter occupies more than one space, the qualifying renter is subject to a corporate entity cap of $300,000. This means that if you are a franchisee or an owner of any chain, the total assistance available is limited to $300,000, despite the fact that your qualifying rent expenses (rent, mortgage interest, insurance and taxes) could far exceed the $300,000 ceiling.

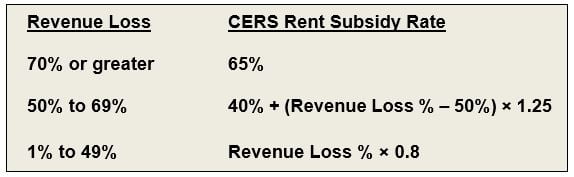

Rent Subsidy Percentage

The rent subsidy percentage fixes the amount of subsidy that an eligible entity may receive to cover its qualifying rent expense in a qualifying period.

The subsidy rate is on a sliding scale. An eligible entity’s position on this scale is determined by the extent to which its revenues have declined:

The greater the decline in revenue, the greater the subsidy available. The Department of Finance Canada has stated that the drop in revenue can be calculated as follows:

Given the aforementioned scheme, it is possible that an eligible entity will have to pre-pay rent in order to receive CERS. The suggested calculation measures the decline in revenue only after the qualifying period has started or ended. Further, each application for CERS must be submitted within 180 days after the end of the qualifying period. We will monitor this as more information comes out from the CRA.

Below are a few examples that demonstrate how CERS provides a level of support that is proportionate to the loss of business:

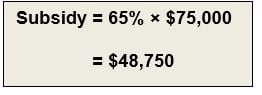

Example A

A single eligible entity has lost 70% of its revenue. It therefore qualifies for the maximum subsidy rate of 65%.

Its qualifying rent expense amounts to $100,000. Because of the cap on expenses, however, the eligible entity would only be able to account for a maximum of $75,000 worth of its qualifying rent expense. It would apply the 65% rent subsidy rate to this upper limit.

The eligible entity would therefore receive $48,750 of support for a qualifying period:

Example B

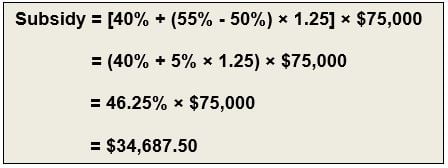

Example B

If the same eligible entity has instead lost 55% of its revenue, the eligible entity would qualify for a lower bracket of support to subsidize the upper limit of $75,000. It would receive 40% of qualifying rent expense, plus 1.25 times the amount of revenue loss above 50%.

In this example, the eligible entity would receive $34,687.50 of support for a qualifying period:

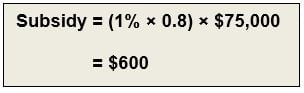

Example C

Example C

If the same eligible entity has instead lost 1% of its revenue, it would qualify for the lowest scale of support. In this case, the subsidy rate would be equal to 0.8%.

The eligible entity would therefore receive $600 in support for a qualifying period:

5. Lockdown Support: What Is the Rent Top-Up Percentage and Who Is Eligible?

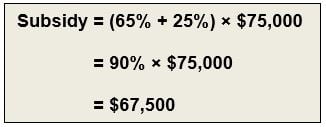

The government is also offering what it calls Lockdown Support: a 25% rent top-up percentage to hard-hit businesses.

An eligible entity qualifies for a top-up if it is subject to a “public health restriction,”[6] an order that is made in Canada in response to COVID-19 that causes the tenant to cease some or all of its activities for at least one week. If it is reasonable to conclude that at least approximately 25% of qualifying revenues were derived from the ceased activities, the eligible entity may capture an additional 25% of support.

In Example A, the eligible entity qualified for a 65% rent subsidy rate to cover $75,000 worth of qualifying eligible expenses. If the eligible entity was under a public health order for the entire qualifying period, it would also receive an additional 25% of support, totaling 90%.

The eligible entity would therefore receive $67,500 in CERS funds:

Importantly, if the public health order is not in effect during the entire qualifying period, the rent top-up percentage is pro-rated to cover only the period in which the order is in place. Further, the $75,000 expense cap applies to the top-up, but the $300,000 corporate entity cap does not.

[1] Bill C-9, An Act to Amend the Income Tax Act (Canada Emergency Rent Subsidy and Canada Emergency Wage Subsidy, 2nd Sess, 43rd Parliament, 2020 [the “Bill”].

[2] Income Tax Act, RSC 1985, c 1 (5th Supp) at s 125.7(1) [ITA].

[3] Bill, supra note 1 at s 2(11).

[4] Ibid at s 2(8).

[5] Ibid at s 2(11).

[6] Ibid at s 2(11).

The information and comments herein are for the general information of the reader and are not intended as advice or opinion to be relied upon in relation to any particular circumstances. For particular application of the law to specific situations, the reader should seek professional advice.